Artist Impression

Now Available

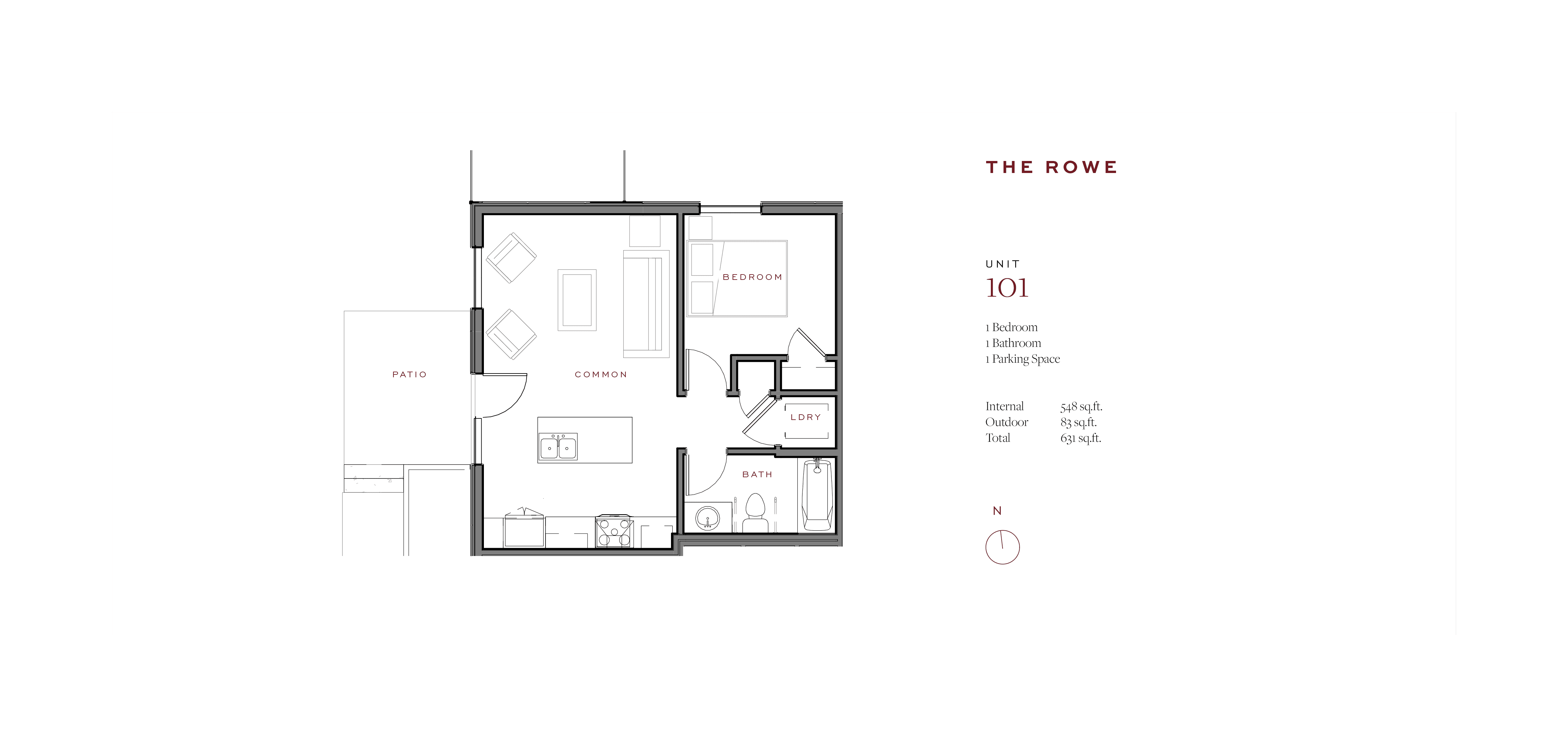

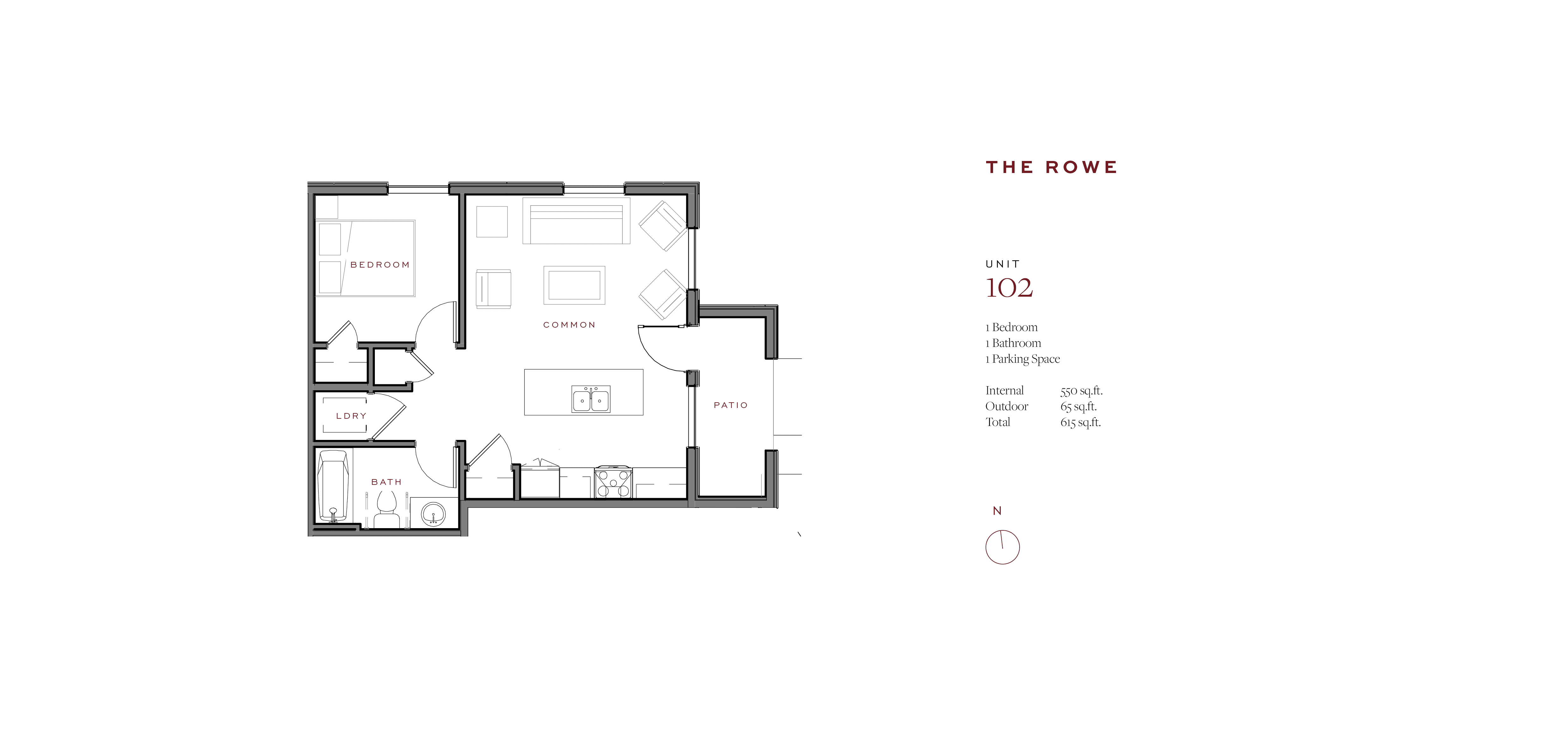

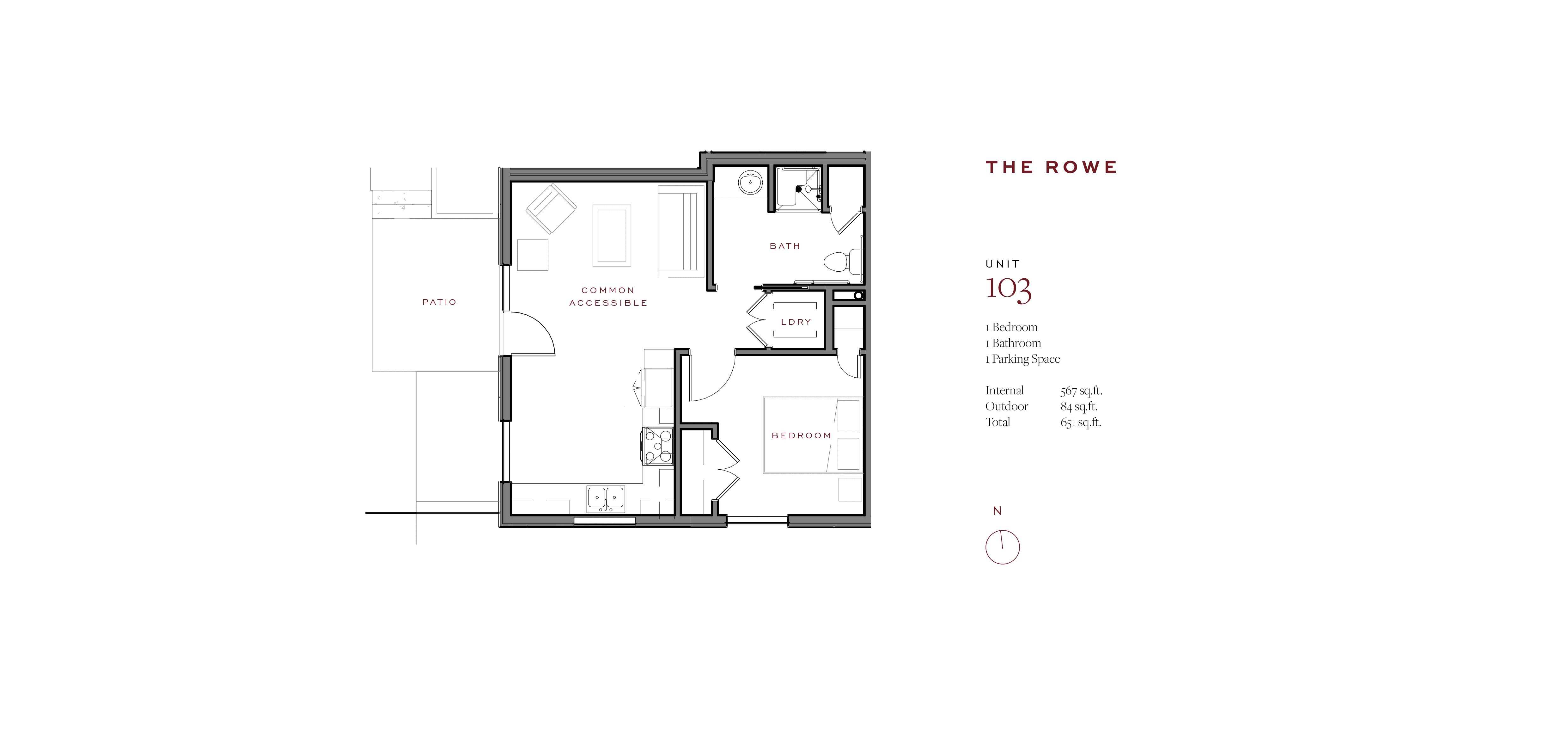

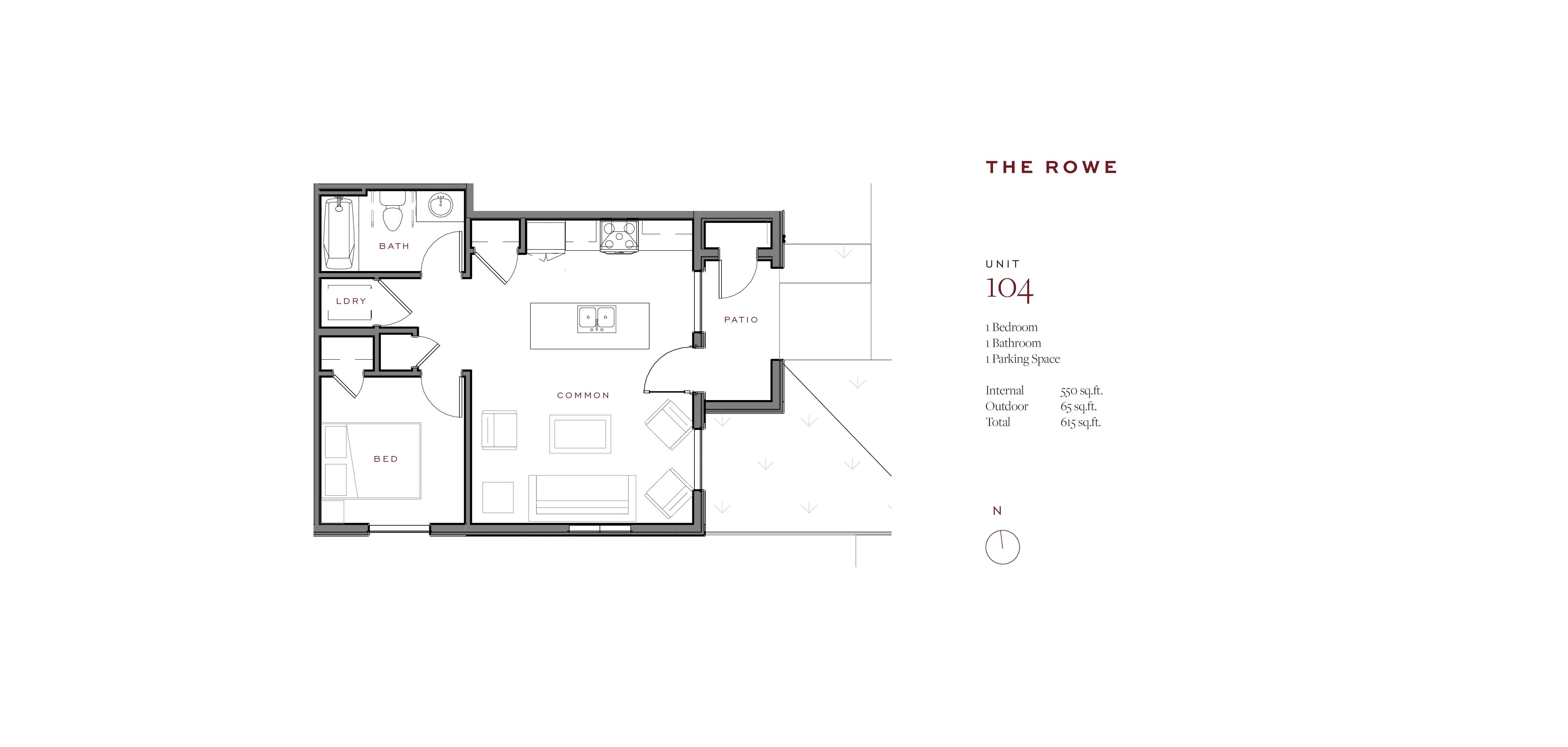

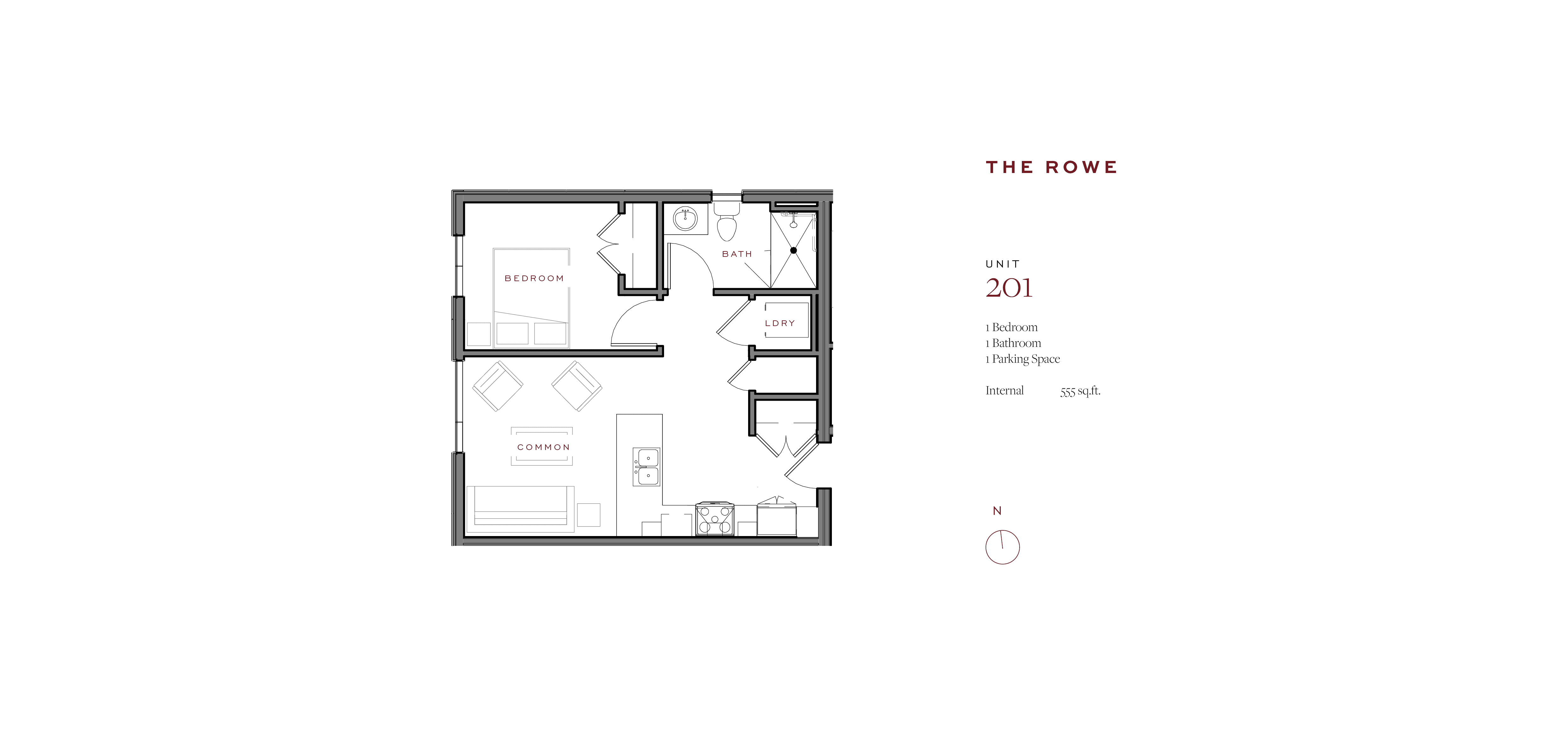

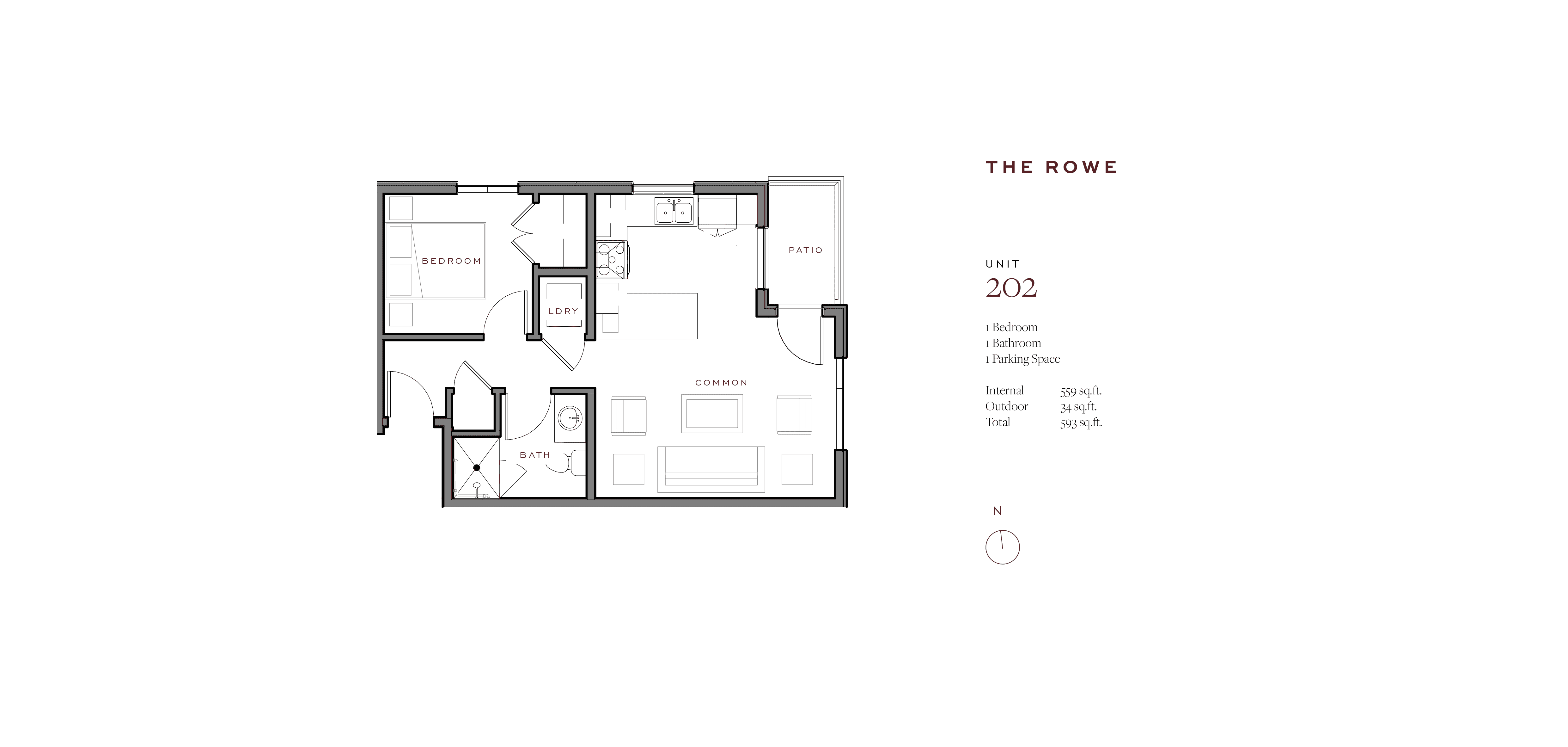

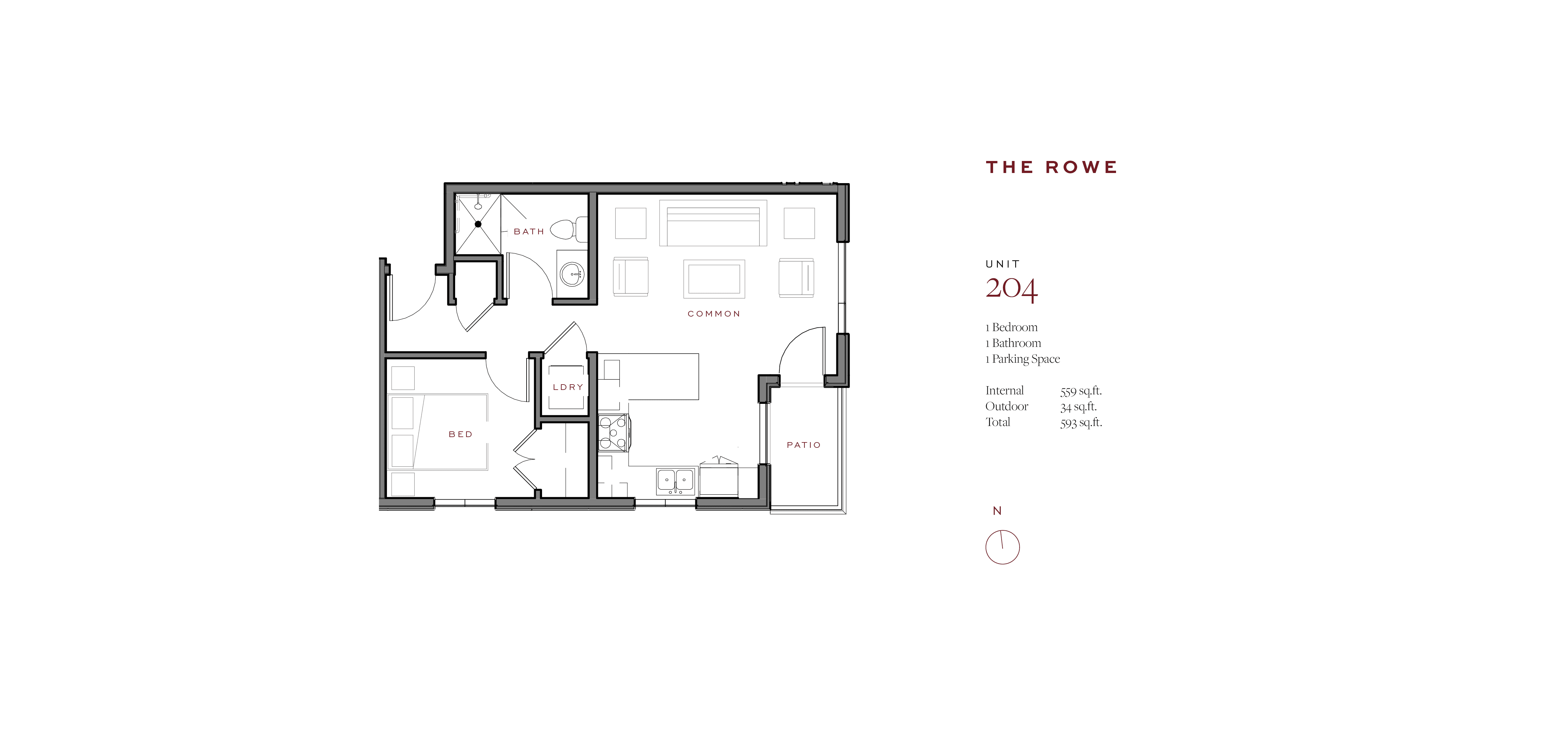

1 Bed, 1 Bath, 1 Car units — $279,000

The 8 permanently affordable units within The Reed are now available for sale. With varying sizes of 548 – 567 square feet, all units are 1 bedroom, 1 bathroom, and include a parking space & detached storage unit measuring 4.5’ x 5.5’ x 8’. Designed for compact, efficient living in Missoula’s coveted University District.

Artist Impression

Vision

—

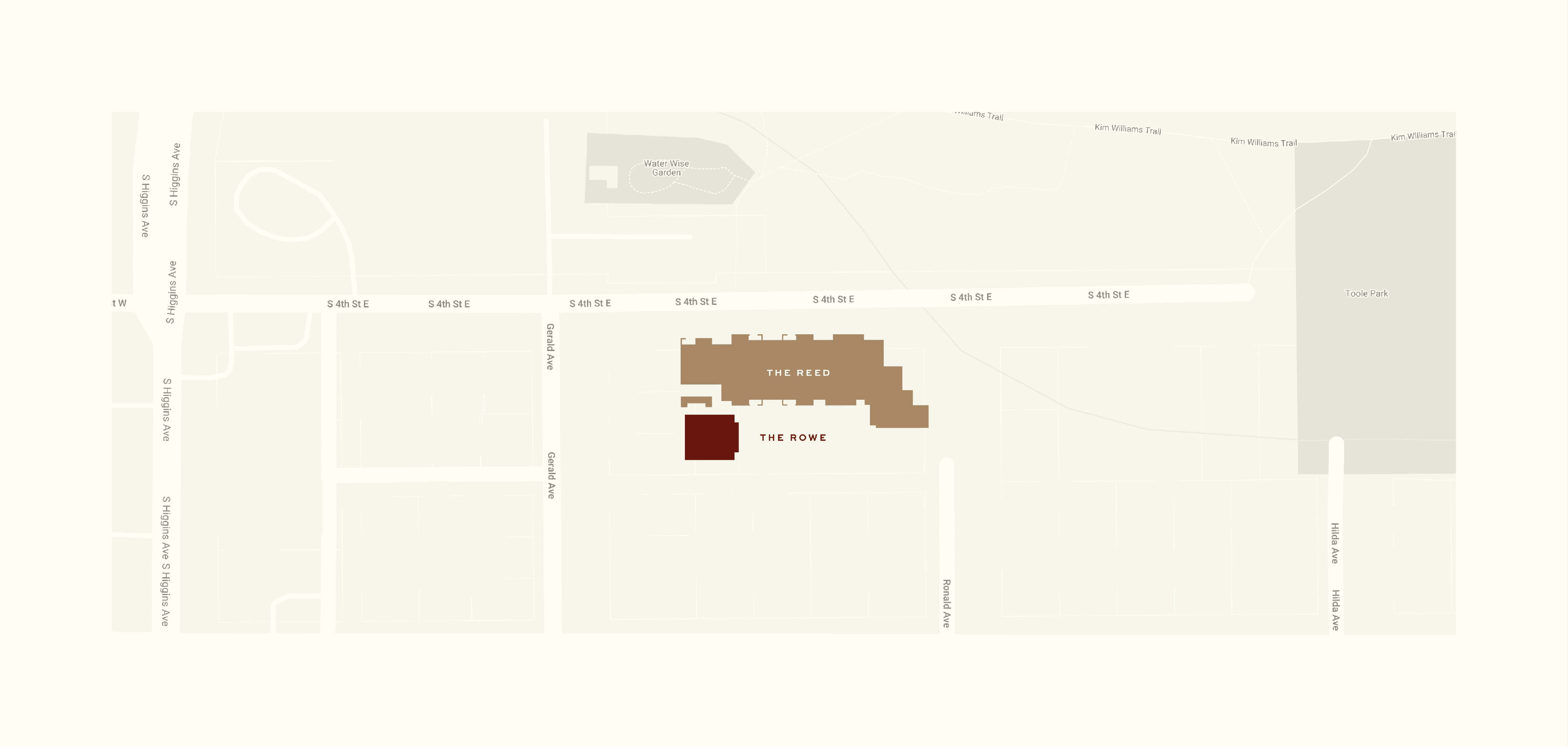

The design intent is to celebrate place, seizing the astounding views of Missoula and the Clark Fork River while being conscious of the City fabric. The building simultaneously increases housing density and pays homage to the historic homes in the area through materiality and a public walkway with interpretive signage to celebrate the past. The façade steps in and out along the main street to reduce the scale and create visual interest, while carving out privacy for residents. The extensive use of brick brings context to downtown and historic Missoula, which is only a short walk for the building residents. We strive to create a structure that fits in well with Missoula, being conscious of the City’s past and future.

Interiors

—

Our vision for the interiors of The Rowe is to offer an experience true to Montana, but with a chic urban edge. We will support a connection to nature in a uniquely refined manner. No other interior in Missoula will offer this level of design and relevance. We will use materials that will complement the expansive views and natural light.

Artist Impression

Artist Impression

Artist Impression

Artist Impression

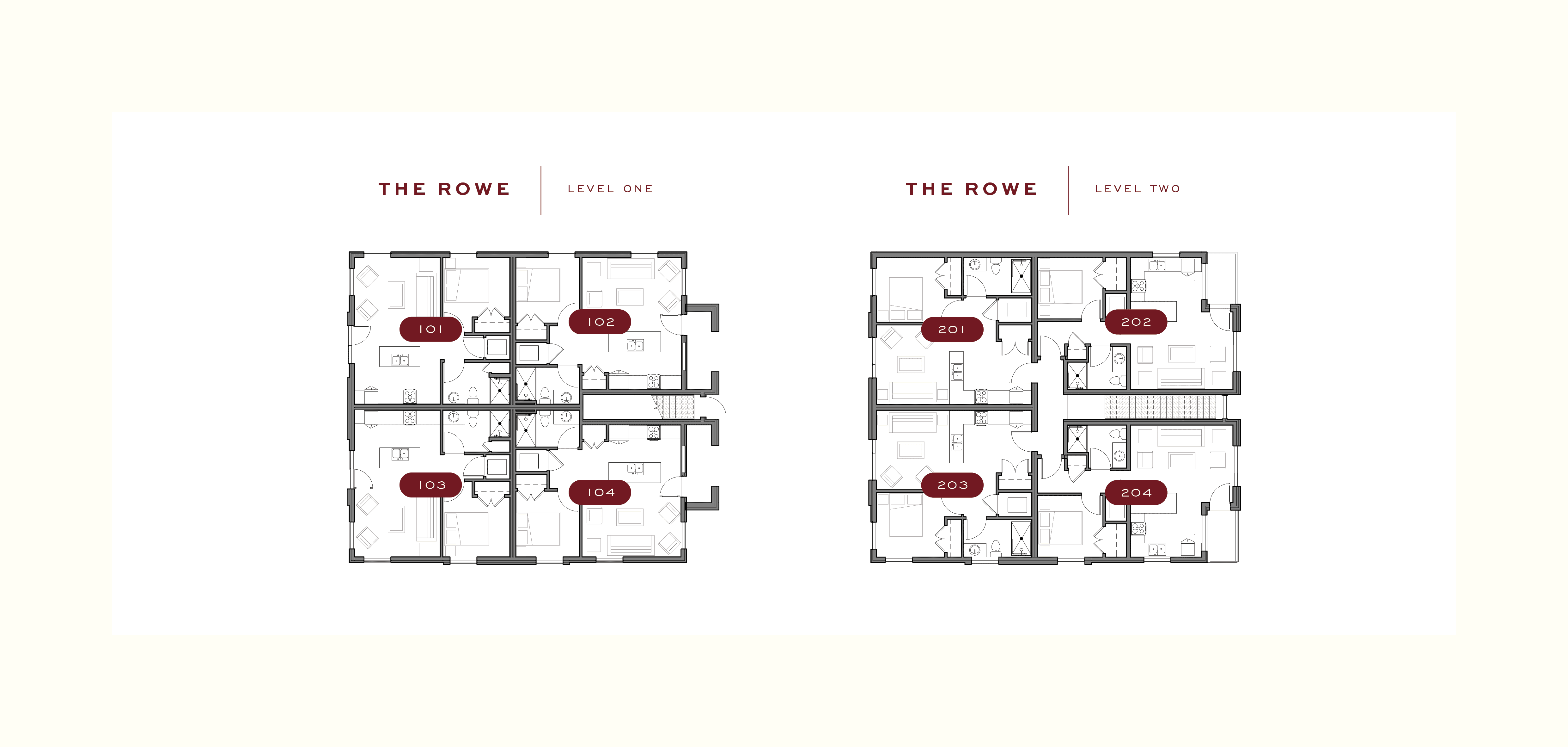

The Rowe Floorplans

The Rowe Level Plans

Permanently Affordable Residences

How are the Rowe Condominiums different from market rate homes?

- The homes are made permanently affordable through a use restriction program, managed by the North Missoula Community Development Corporation (NMCDC).

- Buyers must be income-qualified to purchase a Rowe Condominium. In exchange for an affordable purchase price, buyers agree to pass on the affordability to the next homeowner if they ever decide to move on.

- If and when a homeowner sells their home, they keep all of their earned equity (what was paid off on the mortgage instead of to a landlord), and 1.5% per year of the unearned equity (the market increase). The sale will be facilitated by the NMCDC.

- Homeowners must designate their home as their primary residence.

Artist Impression

Artist Impression

Artist Impression

Artist Impression

Artist Impression

How to purchase a Rowe Condominium

Step 1:

Confirm your eligibility!

You are eligible to purchase a Rowe Condominium if:

-

Your gross household income is below 120% of the area median income, adjusted for household size (see table below)

-

Your household has the ability to deposit $2,500 in earnest money when contract is accepted

-

Your household’s non-retirement assets do not exceed $100,000 at time of purchase. This does NOT include down payment.

- Large down payments and/or gifted down payments are allowed

- Cash purchases allowed if program guidelines are met

-

Your household does not own any other residential real estate at time of purchase

-

Your household intends to live in home as primary residence

-

Income limits by household size

% area median income

1

2

3

120%

$68,640

$78,360

$88,200

-

Are your assets below the cap?

-

Assets to be considered include:

-

Cash savings, including but not limited to bank accounts, credit union accounts, certificates of deposit, and money market funds

-

Marketable securities, stocks, bonds, and other forms of capital investment

-

Inheritance and insurance payments received in the past five years

-

Settlements for personal or property damage received in the previous five years

-

Other personal property that is readily convertible into cash.

-

-

-

-

The following assets are not considered assets by the NMCDC:

-

Ordinary household effects including furniture, fixtures, and personal property that is not readily convertible into cash

-

IRAs, pensions, investment accounts, etc. that would require a penalty for early withdrawal

-

Automobiles used for personal use.

-

Balances in specifically designated retirement funds and college savings accounts

-

Securities, stocks, bonds, and other forms of capital held in a tax-deferred retirement plan recognized by the Federal Internal Revenue Service

-

-

For questions, please contact Brittany at the NMCDC, brittany@nmcdc.org

Step 2:

Get prepared for potential purchase!

Eligible and ready to apply? How to get prepared:

-

Get pre-approved for a loan by Rob Vallance at Opportunity Mortgage (rvallance@oppbank.com) or a lender of your choosing.

- Submit your application to the NMCDC. Download the application below. Then follow the directions on the application.

-

If you have not already, sign up for a homebuyer education class that will detail additional steps in the homebuying process and is a requirement for moving forward with purchase.

For questions, please contact Brittany at the NMCDC, brittany@nmcdc.org

Step 3:

Submit a Preliminary Application and Pre-Qualification Letter!

Download and fill out a Preliminary Application using the link under Downloadable Resources below. Submit the preliminary application and a pre-qualifiaction letter from a lender to the NMCDC according to the directions listed in the application. Applications will be reviewed on a rolling, first-come, first-served basis. If your preliminary application is approved, the NMCDC will reach out to you with information on how to complete a full application and move into the purchase process

In order to prioritize Missoula workers for whom market-rate homeownership has not been feasible, and those who have been waiting for a shared equity home to purchase, applicants with the experiences listed below will receive the following additional entries:

-

50% of household income is earned in a Missoula City/County zipcode – 5 additional entries

-

100% of household income is earned in a Missoula City/County zipcode – 5 additional entries

-

Household has been on a CLT interest list for at least six months – 5 additional entries

For questions, please contact Brittany at the NMCDC, brittany@nmcdc.org

Step 4:

Enter into the purchase process!

Qualified households who complete a full application will choose the unit they prefer and enter into a buy-sell agreement.

Potential buyers will have two weeks to complete the full application. This application includes an evaluation of household income, and the following will be requested:

-

Tax forms and pay stubs to qualify household income at 120% AMI or below.

-

A copy of the applicant’s pre-approval letter from a lender that indicates the address and price of the home.

-

Cash assets verification using two months bank statements and household self-reporting.

-

Buyers must connect with an attorney who can review the deed restriction and answer any questions.

-

Buyers much schedule a 30-minute orientation to the NMCDC’s program with the Land Stewardship Program Manager.

-

Buyers must connect with Homeword to schedule a HUD-approved first-time homebuyer course.

For questions, please contact Brittany at the NMCDC, brittany@nmcdc.org

Downloadable Resources

The following resources are available for your convenience

Qualification And Summary of Restrictions

Artist Impression

Artist Impression

FAQ

Can an owner of a Rowe Condominium choose to sell their home at any time?

Yes. Homeowners just need to give the NMCDC a notice of intent to sell so the next income qualified buyer can be determined.

How much can I sell my Rowe Condominium for?

At resale, homeowners may sell their home for the original purchase price, keeping the equity earned by paying down the principal balance on their mortgage (instead of to a landlord). Additionally, they may receive 1.5% per year of homeownership. The resale formula is dictated in the deed restriction document. Some capital improvements may be able to be rolled into the sale price, but must be approved in advance by the NMCDC and in alignment with the deed restriction document. This agreement allows homeowners to build equity and enjoy stability and affordability while keeping the home affordable for future income-qualified buyers.

Are Rowe Condominiums inheritable by designated heirs and beneficiaries?

Yes. If the designated heir is a spouse or common law partner residing in the home, NMCDC will consent to this person assuming ownership of the home. Any other beneficiary must be income-qualified by NMCDC and, if this person does not meet these income qualifications, the home will be resold at the resale-restricted price and the beneficiary may inherit the proceeds.

Do Rowe Condominium homeowners pay property taxes?

Yes. Homeowners enjoy the benefit of public services like roads, schools, etc. so, like other homeowners, are responsible for paying real estate taxes.

What are the responsibilities of Rowe Condominium homeowners?

Homeowners are expected to be responsible neighbors and community residents. Homes must be used responsibly and for residential purposes. As good neighbors, Rowe Condominium homeowners are responsible for their behavior and for the behavior of any of their visitors. Homeowners are expected to maintain and repair as needed their homes and outdoor spaces.

May Rowe Condominium homeowners rent out or sublet their homes?

Homeowners must live in their home as their primary residency, occupying their home for at least 270 days per year. They may not rent out their home except for in special circumstances, which must be approved of by the NMCDC Board of Directors. Special circumstances may include leaving town temporarily for a work or schooling opportunity, or to take care of a family member.

Are there fees paid by Rowe Condominium homeowners?

Yes. Homeowners pay a monthly ground lease fee to the NMCDC. This fee is $30 per month and can be increased by 10% annually. The NMCDC uses the fees collected to maintain contact with homeowners and provide support and technical assistance as needed, in addition to expanding the offerings of permanently affordable housing opportunities in the Missoula community.

Is there a Rowe Condominium HOA?

Yes. Rowe homeowners will be a part of the broader Reed/Rowe Development HOA. The dues collected will be used by the Association to maintain and manage the development’s common areas, including green spaces, snow removal, garbage, recycling collection, etc., and to replace roofs and siding when necessary.